“Use only that which works, and take it from any place you can find it.”

– Bruce Lee, Martial Artist

Warren Buffett has been one of the most successful investors of our time. He is equally good at distilling complicated investment concepts and explaining them in a way that is accessible to everyone. In this year’s Berkshire Hathaway annual report, he presents a clear and simple argument for long term stock investments being more stable and less risky than long term bond investments.

The core of the argument is that bond investments are fixed to a currency and that paper (fiat) currencies, over the long term, erode in value due to inflation. The purpose of stock market investments is to protect your purchasing power over longer periods of time, such as a retirement of 30 years or more.

We have played with some numbers to demonstrate this investment concept using the 50 year time period that corresponds to the time Warren Buffett has run Berkshire Hathaway. These numbers are all in US dollars to demonstrate the concept. It is harder to replicate in Canadian dollars, since the TSX index did not even come into existence until 1979.

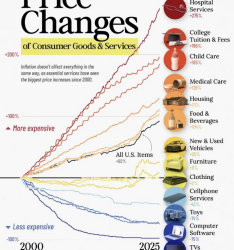

[visualizer id=”964″]

For every $1 you had in 1965, it would take you $7.69 in 2015 to have an equivalent level of purchasing power.

Likewise for every $1 you invested into the stock market in 1965, your investment would have grown to be worth $52.43 – assuming you held your investment and reinvested your dividends over that period.

The idea is that if you used the stock market to improve your purchasing power for 50 years, you can now afford 5 Ford Mustangs (at today’s base price of $23,800) for every one you could have purchased in 1965. Today’s car is also a fair improvement in comfort and safety.

Food items, which are commodities, should closer reflect inflation. We can now get 14 dozen eggs for every one dozen bought in 1965. Here, we would point out that 50 years ago eggs were likely more organic than today’s industrial variety, so conceivably we should be using the $5.00 per carton variety found at Whole Foods. Regardless, the concept still holds.

We have included below a full excerpt of page 18 on the Berkshire Annual Report, so you can read Warren Buffett’s own words. It would be hard to write any better about the essence of the core relationship between balancing exposure between stocks and bonds and understanding their comparative risks.

At Avenue, this long term understanding of risk is exactly the key concept behind our asset allocation decisions process for each of our clients. The starting point is that every one of our clients should be 100% invested in the stock market for the long term. However, if you need some of your money to live on in the near term, we like to have at least 5 to 7 years of fixed income to cover annual income needs. Alternatively, if an individual is uncomfortable with the fairly common stock market swings of 25% or more that the stock market inherently will produce, we can allocate to bonds, but the individual needs to understand that there will be a loss of purchasing power over time.

“Our investment results have been helped by a terrific tailwind. During the 1964-2014 period, the S&P 500 rose from 84 to 2,059, which, with reinvested dividends, generated the overall return of 11,196%. Concurrently, the purchasing power of the dollar declined a staggering 87%. That decrease means that it now takes $1 to buy what could be bought for $0.13 in 1965 (as measured by the Consumer Price Index).

There is an important message for investors in that disparate performance between stocks and dollars. Think back to our 2011 annual report, in which we defined investing as “the transfer to others of purchasing power now with the reasoned expectation of receiving more purchasing power – after taxes have been paid on nominal gains – in the future.”

– Berkshire Hathaway Inc. annual report 2015 (pg. 18), Warren Buffett

The unconventional, but inescapable, conclusion to be drawn from the past fifty years is that it has been far safer to invest in a diversified collection of American businesses than to invest in securities – Treasuries, for example – whose values have been tied to the American currency. That was also true in the preceding half-century, a period including the Great Depression and two world wars. Investors should heed this history. To one degree or another it is almost certain to be repeated during the next century.

Stock prices will always be far more volatile than cash-equivalent holdings. Over the long term, however, currency-denominated instruments are riskier investments – far riskier investments – than widely-diversified stock portfolio that are bought over time and that are owned in a manner invoking only token fees and commissions. That lesson has not customarily been taught in business schools, where volatility is almost universally used as a proxy for risk. Though this pedagogic assumption makes for easy teaching, it is dead wrong: volatility is far from synonymous with risk. Popular formulas that equate the two terms lead students, investors and CEOs astray.

It is true, of course, that owning equities for a day or a week or a year is far riskier (in both nominal and purchasing-power terms) than leaving funds in cash-equivalents. That is relevant to certain investors – say, investment banks – whose viability can be threatened by declines in asset prices and which might be forced to sell securities during depressed markets. Additionally, any party that might have meaningful near-term needs for funds should keep appropriate sums in Treasuries or insured bank deposits.

For the great majority of investors, however, who can – and should – invest with multi-decade horizon, quotational declines are unimportant. Their focus should remain fixed on attaining significant gains in purchasing power over their investing lifetime. For them, a diversified equity portfolio, bought over time, will prove far less risky than dollar based securities.

If the investor, instead, fears price volatility, erroneously viewing it as a measure of risk, he may, ironically, end up doing some very risky things. Recall, if you will, the pundits who six years ago bemoaned falling stock prices and advised investing in “safe” Treasury bills or bank deposits. People who heeded this sermon are now earning a pittance on sums they had previously expected would finance a pleasant retirement. (The S&P 500 was then below 700; now it is about 2,100.) If not for their fear of meaningless price volatility, these investors could have assured themselves of a good income for life by simply buying a very low-cost index fund whose dividend would trend upward over the years and whose principal would grow as well (with many ups and downs, to be sure)…”