Avenue Investment Management has now been looking after client money for 10 years. In this quarter’s letter we will revisit our original purpose and discuss our present challenges. This will be followed by our usual discussion of the current investment climate and how we are positioning our investments for 2014.

The 10 year and 30 year Government of Canada bond interest rates have risen to a level where we believe they will now stabilize. We are again increasing our exposure to interest sensitive stocks and REITS. As global growth returns, resource stocks look like they have bottomed. We can make a rational case for why the stock market will go higher in price but the seeds for the next market correction are being sewn, and again the problem is too much debt.

Avenue’s last Q2 2013 report tried to capture how interest rates needed to go up but because of the weight of government debt, rates were not likely to exceed 3% to 3.5% for 10 year government bonds. Following this argument, the growth rate of Gross Domestic Product (GDP) will remain stuck at about 2.5%. The policy conundrum remains that the U.S. economy cannot hit the magical ‘escape velocity’.

Escape velocity is where the economy can grow at a rate where unemployment can come down to the 5% to 6% level and enough tax revenue can be generated to start to pay down the accumulated government debts. Simply put, if the economy would just grow at 4%, politicians will not need to make any hard decisions to cut previously committed spending.

Interest rates are up significantly since April. However, rates are not that much higher as seen from the perspective of what a company has to pay if they choose to borrow money. We would argue that 80% of the move in interest rates has already taken place. We have started to move our weighting to a more normal level in interest sensitive investments from being underweight. REITS look the most attractive and we have added First Capital which operates outdoor shopping centres across Canada.

From the perspective of Avenue’s Bond portfolio, we are now gradually increasing the term to maturity of the overall portfolio. Up to this point the Bond portfolio has been about as defensive as possible with the average term being 4 years. We have already increased the term back to 6 years and we will consider increasing duration further if interest rates go higher.

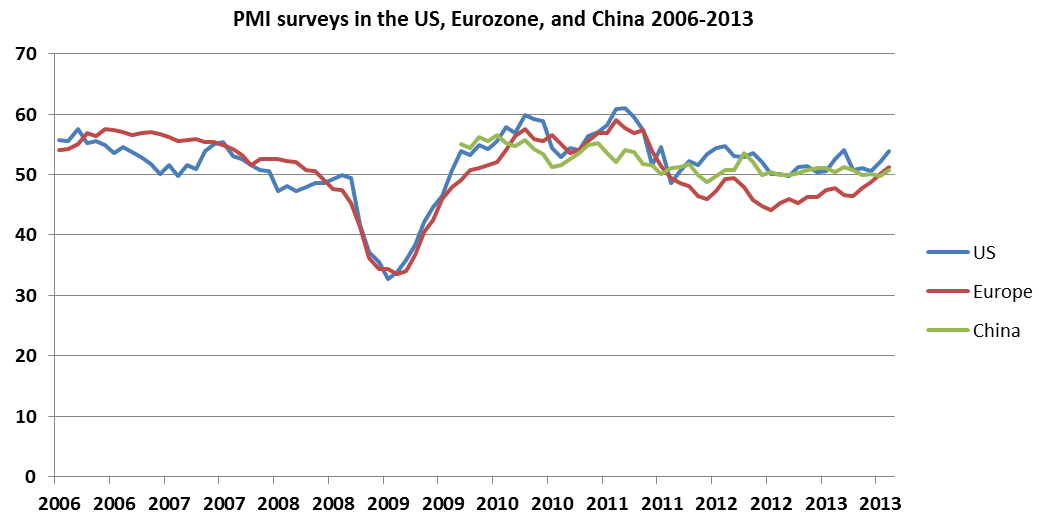

After interest rates, the next theme in order of importance would be a return to global growth for the world’s major economies. The US is now in the rhythm of 2.5% GDP growth. Europe has bottomed and next year will be better than this year. Also, China’s economy looks like it continues to grow at 7.5% which is much better than the credit-starved economic stall anticipated only a few months ago.

All governments are concerned that growth is not stronger. However, for resource investments we just care that the absolute growth number is positive.

A great deal of the rise in oil price is being attributed to the continuing conflict in the Middle East. We believe the price of oil was going to go up regardless. Demand for basic commodities like oil and copper will be 1% to 2% higher next year. We then see a return of investor interest to resource stocks.

We don’t expect it to be as broad based as before but a high quality cash flowing company should be attractive to investors. We have recently fine-tuned a few of the energy investments by selling Cenovus and Baytex to buy Suncor and Crescent Point. We have also added BHP Billiton, a global diversified mining company.

We have just highlighted that the Avenue Equity Portfolio’s investments in interest sensitive and resource stocks should do well. But there is also a strong argument that the overall price earnings market multiple should move higher. With interest rates staying at today’s level, investors will still need to be invested in stocks to accomplish their need for decent returns. So the market price earnings multiple of 15 times earnings that we have had over the last few years should rise to what has historically been a multiple of 18 times earnings in periods when interest rates are this low.

The multiple goes higher because there is no better alternative place to invest. To illustrate, we take next year’s earnings estimate for the American S&P500 index of $110, times a market price earnings multiple of 18 = 1,980 for the index. So the S&P500 Index can still go 19% higher from today’s level.

If we dig a little deeper we will find two more arguments to back up our simple 18 times multiple forecast. North American companies have done a good job paying down debt. For US companies, the debt to cash flow multiple has fallen to 1.7 times today from a high of 3.4 times in 2007. So we now have the healthiest balance sheets that we have seen in a generation.

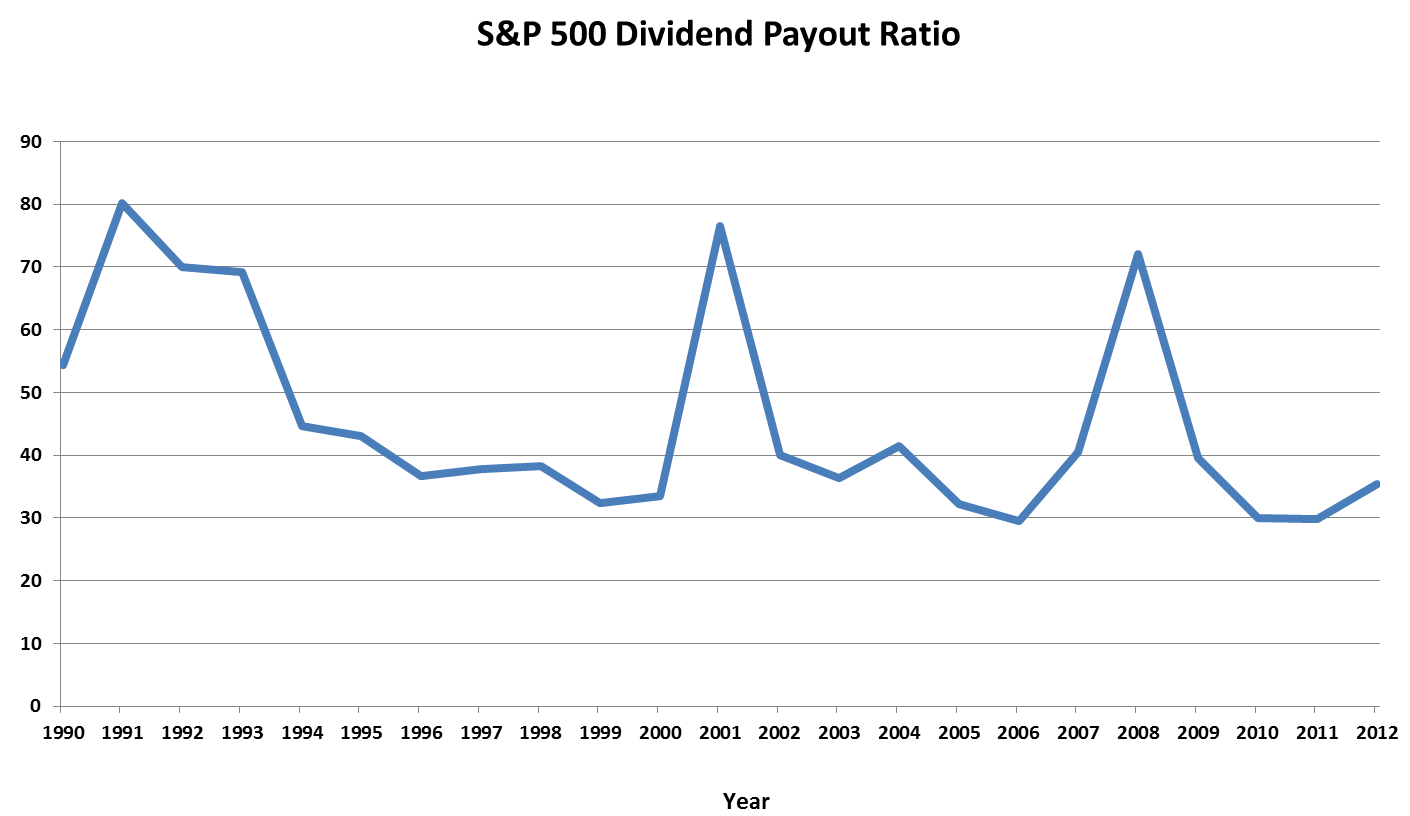

Again, we can pay more for a company’s earnings when we know the business has borrowed a conservative amount of money. As well, dividend increases have not kept up with the increase in earnings. While earnings are not likely to increase dramatically from here, dividend payouts as a percent of earnings should return to more like the historic 50% level. This increase in overall stock market yield will also drive prices and justify an 18 times multiple.

In summary, we continue to have a positive outlook for the businesses we own and we can see that the stock market can move the share prices higher. However, we are now starting to see small pockets of excess that could be the seeds of the next market downturn.

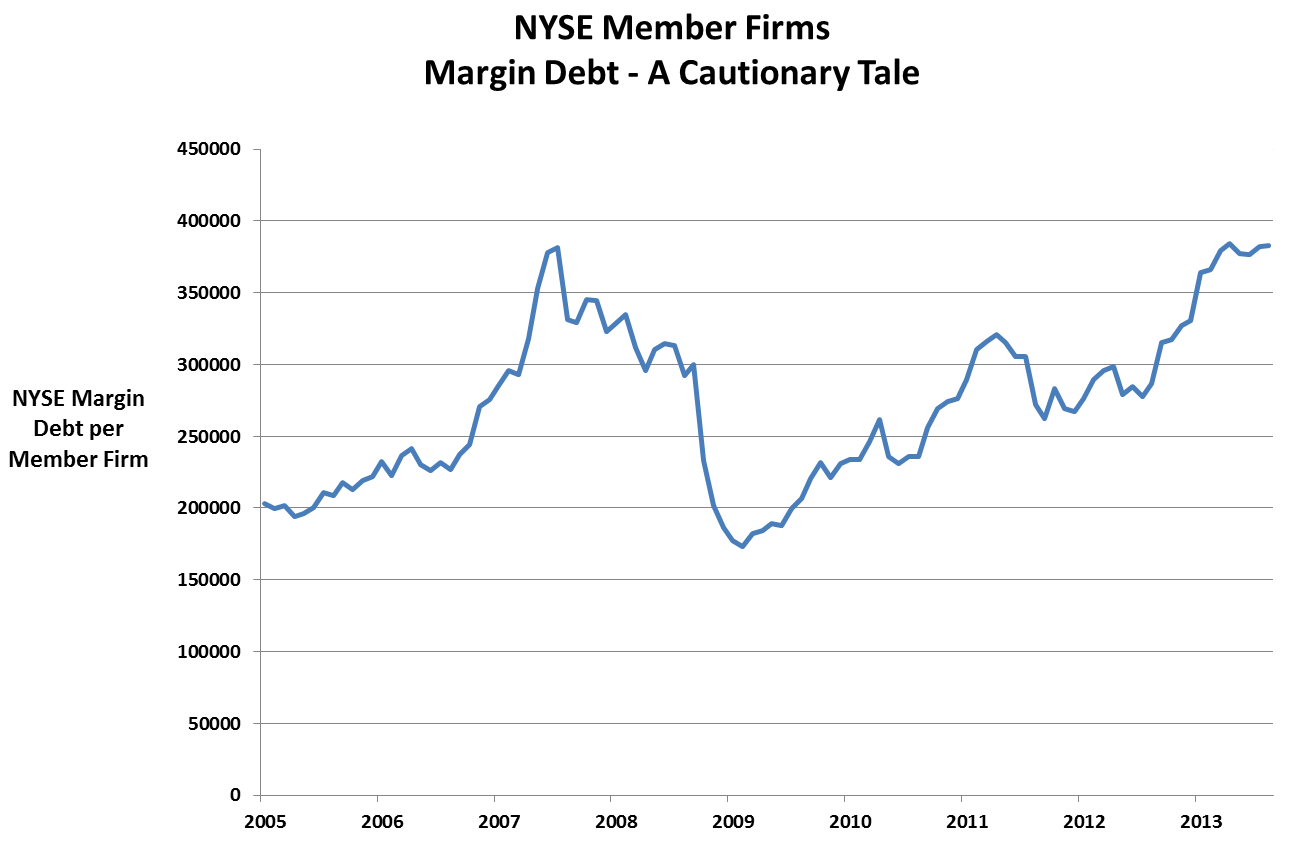

We have noted that companies are conservatively financed, while retail investors are not. Individual investors are now borrowing record amounts of money to invest on the New York Stock Exchange.

Record margin debt does not mean the market is going down tomorrow. How we would interpret it is that when there is the next global destabilizing event, the stock market now has an internal dynamic that will cause the NYSE to go straight down quickly because all the highly leveraged investors will scramble to get out at the same time. When you borrow a lot of money you cannot afford to be a long term investor.

At Avenue, we incorporate the potential for a dramatic market fall into our strategy and make sure we always have cash on the sidelines so we can take advantage of this volatility when it comes. We like the businesses we own but we have to acknowledge that the market is getting inherently more risky and that we have in place a strategy to take advantage of it.