With Canadian bond yields dropping below 2%, these are dark days to be a bond investor. Gone are the days when one could hope for 5-7 % annual returns from the bond market. With global central bank policy using quantitative measures to lower interest rates close to zero, the global $40 trillion-dollar bond market is searching for a “normal” return.

The Canadian bond market is no different, and a disturbing trend has recently surfaced here. As an independent portfolio manager, Avenue is privy to many retail portfolios and we see a persistent trend of reaching for yield without understanding its consequences.

Specifically, attempting to reach a high yield often means investing in preferred shares and private mortgages. The concern is the higher risk that investors are adopting, especially senior citizens, and the regulators seem not to care.

It is now common to see investment advisors using preferred shares as the building blocks for creating a so-called fixed income portfolio for their clients. Most investors are told these shares are fixed income. They are not. Although preferreds are higher on the capital structure than pure equity, they still have inherent risk and they are much riskier than the traditional corporate bonds if one needs to rely on the income they provide. During a company’s restructuring, preferreds are usually “wiped out” with the common equity. Only creditors (i.e. bond holders) hold the cards in the restructuring or bankruptcy process. If there is any inherent value left in the company, the bond holders get the lion’s share of the remaining assets.

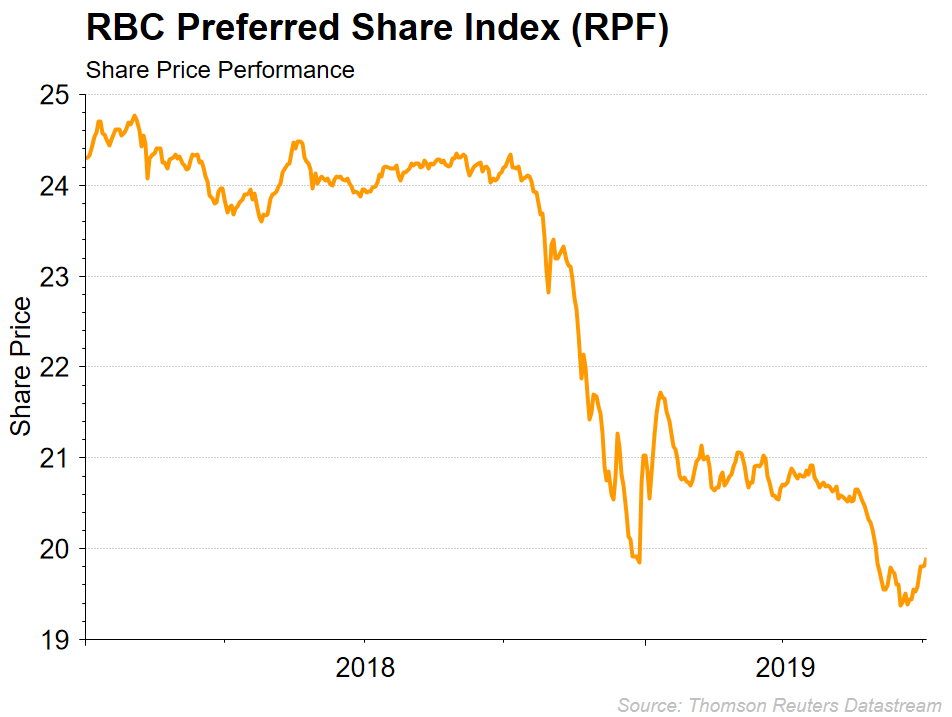

Recently, a more important issue has reared its head for preferred share investors. Here we are talking about preferred shares that have a dividend reset policy. Over the past few years, bank underwriters have issued billions of these shares, close to $5 billion worth of preferreds in 2018 alone. Critically, these issues have a rate reset policy. These were issued as rate-reset preferreds because most analysts believed interest rates would go back up in 2018 and 2019. Therefore, the dividend yield would reset at higher coupon levels since interest rates would increase in both Canada and the US. This obviously did not happen. Dividends are being reset at much lower yields. When that happens, the value of your preferred shares will drop significantly.

Now let’s go back to advisors that are recommending these preferreds. Investors that have these resets are now down between 15-30% depending on the issue. For a retired investor that is looking for fixed income, this is not it. A fixed income portfolio is not supposed to drop 20 – 30%. From an asset allocation perspective, fixed income is about providing stability and preservation of wealth while giving you a stable rate of return. Yes, interest rates are very low by historical standards. Investors will have to accept this fact. What they must not do is chase yield at this point in time.

The same rule applies for mortgages. Many private mortgages that investors hold give some enhanced yield, but the problem is that there is inherent risk with this product. Not only is it illiquid, but in a downturn in the economy these types of investments can drop to close to zero. (Just look at the recent collapse of a prominent mortgage lender where investors lost everything.) Once again fixed income portfolios are not supposed to have these risk profiles.

Please do not misunderstand, preferred shares are a relevant product. Preferred shares have low correlation to fixed income securities and the inherent tax advantage can be compelling in certain situations. The problem arises with the individual investor’s asset allocation and risk tolerance. Many retired investors have these types of products which is fine when you have a 10-20% weighting under normal diversification rules. However, we believe this is frequently not the case. When looking through prospective client statements, we are seeing weightings that are far higher and are inappropriate given the risk tolerance of the investor.

The investment community will have to deal with this fallout. As the chase for yield marches on, investors are looking to alternative investments that have inherent hidden risks. Investors will need to understand the real risks involved and should always be prepared to ask the question – “Why do I own this?”