In Avenue’s equity portfolio, Enbridge is a great example of an investment which demonstrates the current valuation paradox.

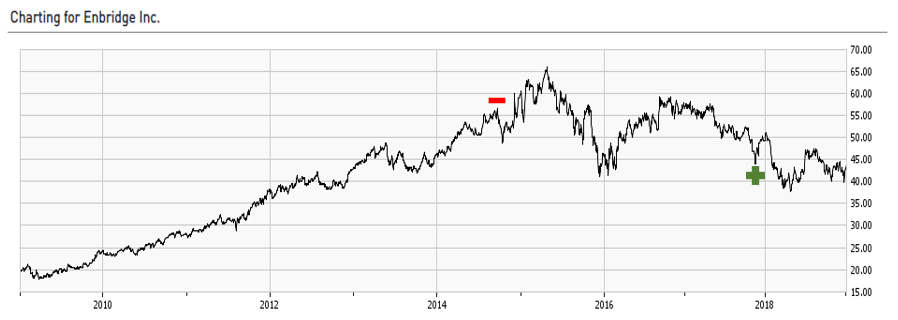

Below is a chart of Enbridge’s share price over the last 10 years and a table showing the increase in dividends and yield over that same period. You can see that today’s 6.7% dividend yield makes the shares the cheapest they have ever been, but still the stock market sentiment is negative on the shares.

We like Enbridge because it has the best pipeline infrastructure in North America. The company that produces the oil pays Enbridge a fee to transport the oil to a refinery. It is a very simple business. The problem for Canadian oil producing companies is that there is more oil than there is pipeline capacity to move it. The handful of projects to add pipelines are stalled, for a number of reasons. This does not change the fact that Enbridge has lots of existing pipelines and they are all full and making money. We as investors get a great long-term income stream from what is a comparatively stable business.

The criticism for owning Enbridge is that the company cannot grow and therefore cash flow and the dividend will not grow either. This argument ignores the fact that the dividend has grown from $0.74 per share annually in 2009 to $2.95 annually for 2019, an increase of 300%.

With the current 6.7% dividend, the company doesn’t have to grow that much for us to hit Avenue’s 8% compounding target. Again the 8% rate of return allows us to double the value of the investment every 10 years. The more important part of the compounding equation for us is that Enbridge remains profitable and this is what we will be monitoring carefully.

We would also like to point out that we have reduced the holding once over this 10-year period when we believed the stock was expensive. A little too soon as you can see. We then doubled the position in late 2017 at a price where we felt the underlying value had caught up to the share price. We don’t see any signs that the profitability of Enbridge is deteriorating. We are happy to own it at this level and capture the income stream that can then be used to reinvest into other holdings and compound the portfolio.