Avenue’s stock market investment strategy is to find business that have consistent earnings and trade at a fair price. Technology is difficult to fit into these parameters because technology companies by nature have disruptive business models which don’t always result in consistent earnings. Our topic today is to show just how expensive and erratic many of these technology companies have become. We will examine the influence of Softbank’s Vision Fund and WeWork on tech venture investing.

Softbank’s Vision Fund is a pool of $100 billion dollars which has emerged as one of the biggest global venture capital investors. It is the largest investor in household names like Uber, Slack, Didi (the Chinese equivalent of Uber), and WeWork. And it is the withdrawing of WeWork’s initial public offering (IPO) and the trail of wild valuation swings that make it a timely example of extreme valuation in technology investing.

Who is behind Softbank’s Vision Fund? Is it run by an autocratic portfolio manager named Masayoshi Son. At 16 years old he emigrated from Japan to California and became interested in technology. Through smarts and luck he was an early investor in Alibaba. Alibaba is the Chinese equivalent of Amazon, eBay, and PayPal rolled into one. His initial $20 m Alibaba investment in 1999 has propelled him to the 43rd largest billionaire in the world. He is back living in Tokyo and seen as a technology visionary.

His Vision Fund’s business model is to seed emerging disruptive internet businesses with enough money so that they can become global category killers before they come public. The problem is that in their enthusiasm and early success, valuation and profit are things that don’t seem to matter. The question raised is Softbank actually “smart money”?

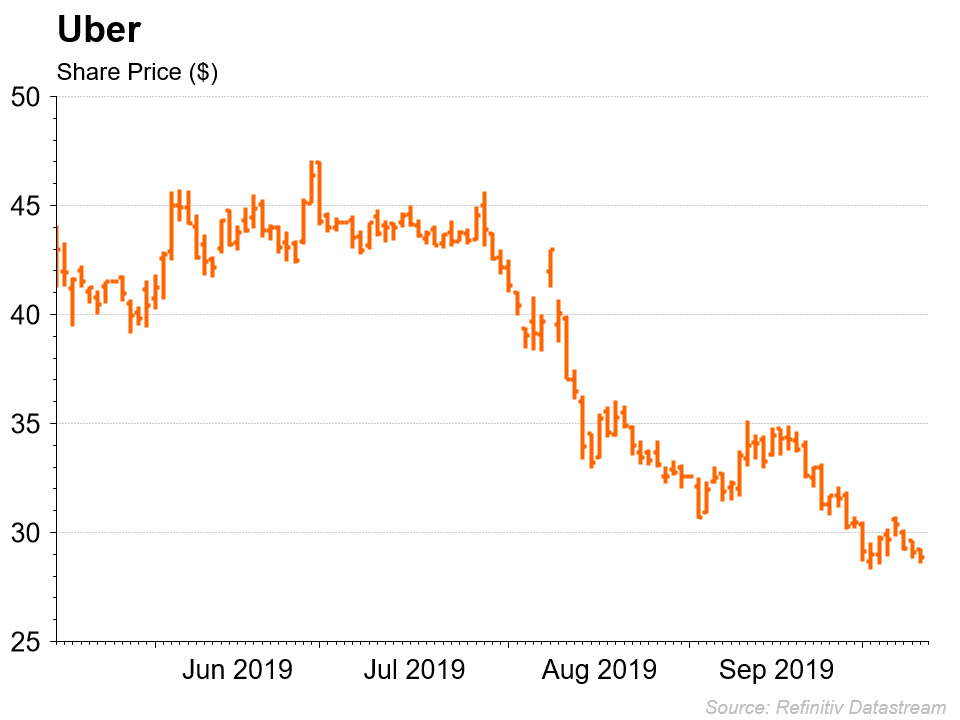

Uber is now a public company and it trades with a market valuation of $50 billion. It has revenue of $11 billion and seems to have a hard time making money. Also, it looks like there is plenty of competition.

In the last few weeks WeWork was expected to become a public company, however, the cancelation of the IPO revealed an extraordinary example of private market overvaluation. WeWork is a global commercial real estate company that provides shared workspaces for technology startups. In summary, WeWork’s most recent private valuation where private investors put money into the company valued it at $47 billion. The company then tried to realize this valuation in the stock market by going public. The initial valuation for their stock was set around $20 billion by investment bankers at the end of the summer. When the bankers actually went to market the company to potential investors, they found that the highest valuation they could get was $10 billion.

WeWork Valuation

How can the private and the public valuation be that different? And more importantly, who’s money is it in the Vision Fund investing to create these crazy valuations and get it that wrong? Well, one third is Masayoshi Son and Softbank’s money and the other two thirds are Saudi Arabian and Abu Dhabi sovereign wealth funds. Connecting these dots, it looks like Masayoshi Son’s vision doesn’t really care about hard numbers and with his level of wealth he doesn’t really have to worry. If he loses 90% of his wealth, he will still be worth $2.5 billion. And to be generous, it looks like the richest guys on the block who most want to diversify their wealth away from oil and into the new economy got duped into believing this one guy in Tokyo had all the answers.

WeWork is just today’s example of wild valuation. It really is the scale of money flows that we as investors have to be aware of. Technology investing today is just as crazy as it was in the dot.com era of 2000. Great businesses will be created but quite often more money is being poured into technology businesses than will be ever returned to investors in profits. While the lucky tech titan Masayoshi Son and Saudi Sheikhs can afford to make this scale of mistake, we would prefer not to. At Avenue we will continue to look for investments underpinned by hard asset values and profits.