John Ray’s handbook of proverbs, 1670

In this quarter’s letter we would like to discuss Avenue’s investment strategy in relationship to the current strong overall performance of the stock market. We believe a balanced portfolio of high-quality consistent businesses is more important than ever. While interest rates may rise further, proportionally most of the move has likely already happened.

One of the obvious challenges with investing is that it is easy to make mistakes. The stock market prices are set by all investors collectively guessing what a company’s profitability will be at some point in the future. In hindsight, it seems easy to have predicted that Central Bank interest rate policy and government stimulus spending throughout 2020 would bail out the stock market. The big mistake we could have made last year was to be overly cautious in April. Any money on the sideline from that period has experienced a significant opportunity cost.

‘A bird in the hand’ is at the core of Avenue’s investment strategy. This age-old proverb expresses the idea that it is better to have a lesser yet certain profit, than the possibility of a greater one that may come to nothing. At any point in time, there are always many future outcomes. It is very difficult to continually guess which stock or sectors within the stock market will outperform all the others.

We believe that we have built a portfolio to achieve our goals no matter the economic environment. Our strategy at Avenue starts with putting constraints on the types of businesses we like to invest in. These constraints are designed to keep us out of trouble. We never start looking at a company and how much money we can make without first considering how much money we can lose if we are wrong. We look for assets or circumstances that can minimize the downside when we assess the underlying business. As we have repeated many times, we like to find investments with a consistency of profitability where the underlying business can compound on its own and then, of course, we don’t want to pay too much for it.

Building a portfolio of profitable businesses with balance across all parts of the economy protects us from the random collapse of any one sector. As we also pointed out in last quarter’s letter, there is now extreme concentration risk in a handful of technology stocks. These are certainly all amazing companies but their stocks’ valuations are now very expensive. And one thing we do know is that technology is always evolving. But more on that topic a bit later.

Lastly there is the constant reality that the stock market is prone to the occasional swoon. With low interest rates, high valuations and herd mentality the risk of another drop is increasing. Waiting for the drop to invest is also not a viable strategy given that it can be years if not decades between events. We will miss out on all the compounding of dividends. So that is why we introduced the Avenue Tail Protection portfolio last year as a perfect complimentary strategy to combine with Avenue’s portfolio of long-term investments. We believe we will make money with the hedge in a down market and be able to use these profits to increase our position in our favourite companies when they are trading at depressed prices.

2020 Hindsight

While we want to spend most of this quarter’s letter discussing where we are going, we think it is still worth understanding what happened economically in the last 12 months. It is not an exaggeration to state that we have never seen anything like this before. 2020 was something very different than a recession or depression. A portion of the economy, estimated at about 15%, was completely shut down, while the rest of the economy functioned more or less as normal.

We were able to make this argument last year, but now we can now see it in the numbers. Canada has a modern industrial and service economy. Throughout 2020, industry kept running and services like lawyers and accountants were able to pivot into the digital age. Consumption of home items surged. It is the services where we spend our disposable income, like restaurants, concerts and travel that took the hit from an economy in lock down. The result was a dramatic increase in personal saving. Savings don’t go up in a recession. We don’t, as of yet, have a definition for this type of economic outcome created by the pandemic.

Will this be the roaring 20s again?

2021 has many qualities that could result in a continuing surge in stock market speculation. Most households have excess savings and pent-up demand while Central Bank policy intends to keep interest rates low for at least the next two years. While we need to stay invested, we also want to avoid what have become obvious pockets of excess.

There is now a feeling among investors that the recovery was inevitable and asset prices will keep rising. The suppression of interest rates has also suppressed two fundamental parts of capitalism: price discovery for the level of interest rates and moral hazard where now it is unacceptable for businesses to fail. The view that the stock market only goes up has become imbedded in investor psychology. While the trend and fundamentals point to higher prices, we still need to have an eye on the horizon to see if there is a storm coming.

One such decade-long tailwind for corporate earnings will become a head wind in 2021. We wrote optimistically in 2009, coming out of the 2008 financial crisis, that there existed the best fundamentals for stock market bottom line earnings. We felt, at that time, that the economy would recover, costs were contained, the cost of borrowing would stay low for longer and taxes were going lower. At this time period, when we assess the earning recovery post pandemic, revenue will recover but operating costs like raw materials are up, the cost of borrowing is going up, and taxes look like they are going up as well. The result is margins that are lower than investors might have forecast. We must be mindful of the type of businesses we invest in and assess whether they can navigate these changes. Most importantly, this will be a headwind for stocks with expensive valuations.

As well, Central Bank and Federal Government stimulus have had a dramatic and distorting effect on asset prices. When interest rates are this low, investors are willing to pay more for earnings that might happen in the distant future. What are commonly called growth stocks will get a high valuation based on the expectation of future earnings. It is just a reflection that since interest rates are so low, borrowing money has little cost.

With interest rates going up in the last few months, this trend has reversed slightly. Companies that have stable earnings today become more valuable than companies that might make a lot of money in the future. We believe our portfolio of businesses with quality earnings, which still trade at reasonable valuation, is in a sweet spot.

Is inflation coming back?

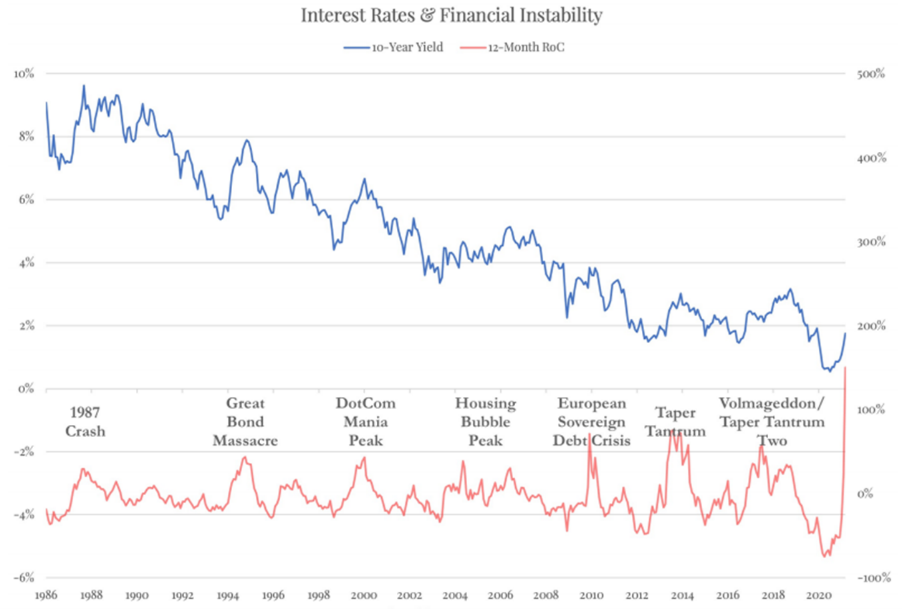

In Avenue’s year end letter, we wrote that we had positioned the bond portfolio defensively given the need to protect our good return in 2020 and given our view that interest rates might go up. We even stuck our neck out with a forecast that inflation expectations might increase to 3% by the end of 2021. Three months later, 3% consumer price inflation is now the consensus estimate for the year.

The benchmark US 10year treasury bond has gone from a yield of 0.5% to 1.7% in three months. And while 1.7% is still a low interest rate in absolute terms, financial markets are very sensitive to the rate of change. The way financial markets see it, the US 10year treasury bond’s yield increased a record 240% in just three months.

Avenue’s bond portfolio was down in Q1 but only by -0.5% compared to the Canadian bond index which was down -5%. Yields are now at a level where we have started to invest some of the cash in the portfolio. We are focusing on provincial bonds first. We are holding off on buying new investments in corporate bonds given the current prices are still expensive relative to historical levels.

For a more detailed analysis of our inflation expectations, please see this month’s Case Study on Inflation vs the Velocity of Money.

Why is technology investing difficult?

Technology businesses are fantastic investments because they are what is called asset light. Once you have your computer code and defined purpose it is easy to replicate at scale. In contrast a lot more plant, equipment, steel and labour must go into building cars and planes.

However, technology businesses are difficult to predict because it is hard for a company hold on to a dominant market position in a hyper competitive market with access to what seems like unlimited investment capital. Additionally, high margin and asset light companies now trade with high valuations which don’t given us any room or margin of error if the future is not as bright as expected.

This time last year, we would certainly not have argued against the idea that big technology stocks like Apple and Microsoft could go to new highs. But to be clear, such a forecast would be saying: this expensive Apple stock is going to become a really expensive Apple stock. A likely possibility, but then what do we do next? You can then see how easy it becomes to start jumping from expensive stock to expensive stock while speculating on where the flow of money is going to go to next. Instead, we believe it is more productive to concentrate our research efforts on finding technology businesses that have lots of room to grow and have a reasonable valuation. Buying a technology stock at a reasonable valuation is no different than buying any other stock; a reasonable valuation protects our downside if there is an unanticipated business disruption.

We would like to point out that at this time two years ago, Avenue’s technology investments were BCE, Apple and Microsoft, and made up about 7% of the portfolio. (BCE is now considered technology where previously it was categorized as telecommunication.) Now Avenue’s investments in technology are focused on North American and European software applications comprised of Constellation, Topicus, Enghouse, Roper, CDW and Citrix. These investments make up 12% of the portfolio. Our holdings were slightly higher, but we recently sold our successful investment in the Canadian software services company Dye Durham.

Crypto currencies go mainstream

We are experiencing a profound development in technology and finance. The market value of all crypto currencies is now the equivalent of about $2trillion US dollars. We feel, as do most investors, that we need to understand this emerging asset class and so here are our thoughts.

Crypto currencies like bitcoin, are encrypted lines of computer code that can be exchanged and in bitcoin’s case there is a finite amount. As long as there is perceived value between a buyer and seller, then it is a real thing. It is a basic human trait that we like to collect scarce assets, seemingly even if it is just digital code.

Looking at crypto currencies as a mainstream investable asset is more problematic. Yes, there is a perceived value, but a bitcoin is essentially a thing, more a collectable, like gold or a rare wine. At Avenue we invest in businesses. Again, if we can find a good bitcoin-based business trading at a fair price, we will absolutely investigate it. You can put the equivalent of silver bars or pounds of uranium in your RSP, but then you are purely speculating on the price of the object. At Avenue, our returns are underpinned by the profits of productive businesses.

We would also like to remind ourselves of the two pillars of investing in Western democracy: the importance of private property and the rule of law. It feels like we are moving into an era where these pillars are being taken for granted. At Avenue, our first exercise for assessing any business is if things go badly what hard assets does the company really own that are tangible and of value to someone else. Is there an asset that can be repossessed by the courts?

You can now buy bitcoin quite easily on many exchanges. But Bitcoin is not registered security (Which is the fundamental point of it.) and they do not come with benefits and safeguards like custody and a fully developed legal system. It is unlikely you will be able to go to court and say “hey that North Korean guy took my decentralized string of computer code and I want it back.” And if you do decide to take your code off an exchange, please don’t lose it, but don’t tell anyone your 24 word random password either.

Crypto currencies are exciting to talk about and many businesses might be profoundly changed by the underlying block chain technology. Please reach out to your Avenue team member if you have curiosity about the space.