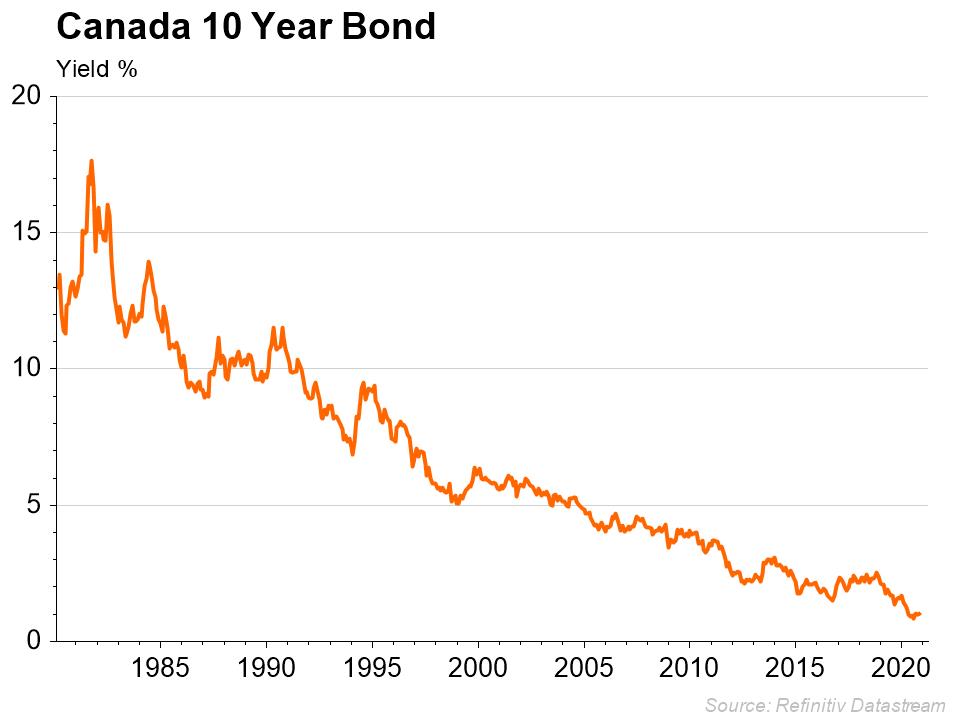

After a forty-year bond market rally from a high of 18% in 1982 to the current 0.70% low today, we struggle to get excited about bonds in the short or medium term.

Now What to Do?

Bonds have always been there to diversify from the volatility of the stock market. The idea was, and is, when stocks go down, bonds go up, and vice versa. In 2020, we saw that historical relationship break. When stock markets crashed in March, the Bond Market went down as well until the Federal Reserve and Bank of Canada “saved” the Bond Market.

Another attribute is that bonds are there for capital preservation despite having little yield, which is a very important attribute to have when dealing with risk or asset allocation of clients’ wealth.

When we look beyond those two benefits, we struggle to find many opportunities in the credit or interest rate market due to historically low interest rates. As well, we have seen the central banks’ interventions into the credit markets suppress credit spreads.

Where Do the $300 Trillion in Global Debt Markets Go From Here?

For the past two decades, analysts, economists and central banks have forecasted incorrectly that global bond yields should yield at higher levels. The ongoing combination of technological disruption, global free trade expansion and our aging population has caused deflationary pressure, therefore causing yields to be suppressed.

Why It’s Different This Time

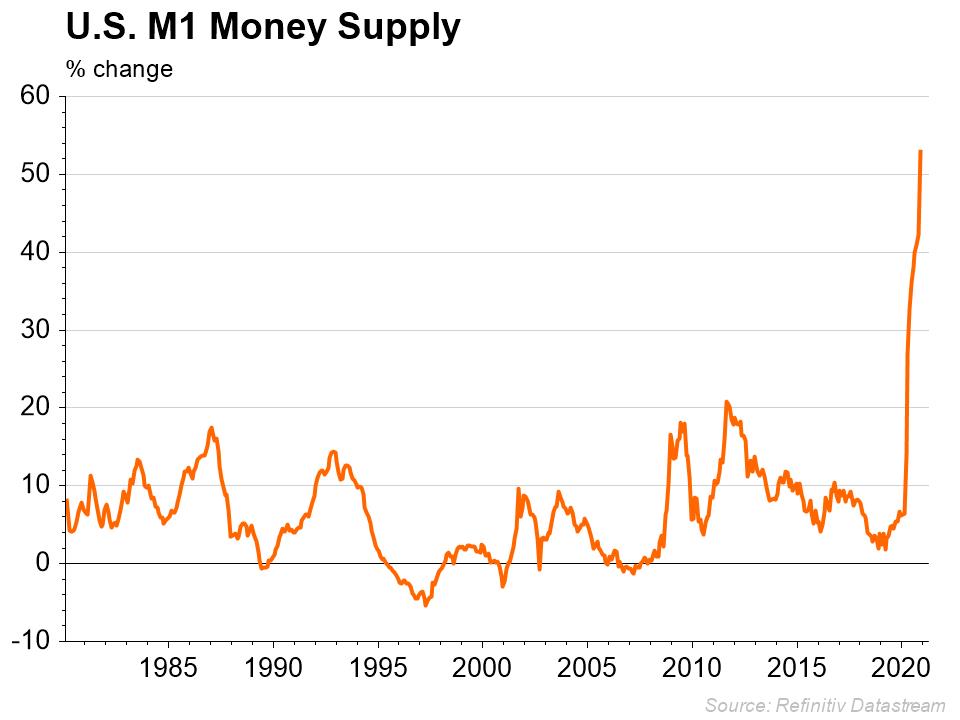

For the past decade, central banks have “pumped” the system with a massive injection of money for two reasons. Firstly, for the public markets to function properly. Secondly, they are trying to keep businesses afloat (large and small). The former worked wonderfully, the latter not so much.

When central banks increase liquidity, they release funds to the banking sector. The problem has been that this money doesn’t leave the bank and get lent out into the economy. The banks are too scared to lend or it is too expensive (from a capital perspective) for them to lend. So, the money never gets into the hands of main street and the commercial banks just buy government bonds to keep on their balance sheets.

For the economy to recover, the commercial banks need to get money into people’s hands. This could happen. More on that later.

The Central Banks are also trying to reflate the economy. To get inflation, you need several conditions in place. Or to say it differently, you need specific ingredients to bake an inflation cake:

1. Central Banks Are Slowly Losing Their Independence

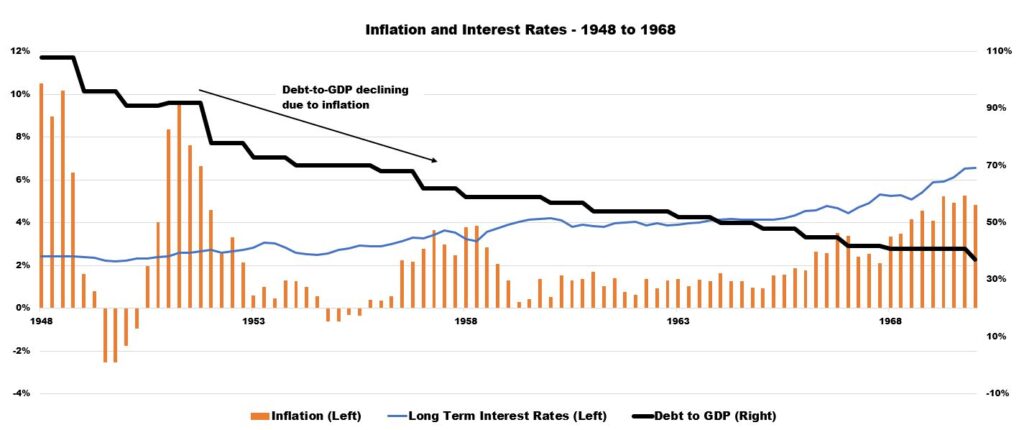

With record amounts of sovereign debt, there is very little chance that central banks will not be influenced politically. There is a view that the only way out is to inflate the debt away. This occurred in 1948. After WWII, the Allied countries were left with a massive amount of debt. They had little chance of paying it back. So, they used inflation as a monetary trick. After the war, there was tremendous pent-up demand resulting from rationing, consumer high savings rates and European rebuilding (Marshall Plan). All this caused inflation over several years. They used higher inflation to lower the outstanding debt since future dollars are worth less than present dollars, thereby dropping the real debt ratios.

2. Labour Market and Class Division

There will be a new agenda focusing on closing the divide between the upper class and the middle class. We have started to see wage increases. As an example, minimum wage workers have seen their wages double. We believe we are going to hear more of new labour union creation for the working class to extract more profits from their companies. An example is the organizing of Amazon workers.

3. Global Trade

a) Modern Trade Agreements and Reshoring

We have seen so much deflation coming from global trade agreements set in the 1990s and 2000s. The Agreements in place are starting to unwind. We are seeing western countries renegotiate trade deals that encompass not only economic benefits but must have social benefits as well, which will lead to higher prices for goods. Manufacturing is also looking to bring back their production to their own country, which is called reshoring. Goods will be more expensive.

b) Cold Trade War with China

Western economies are starting to re-evaluate their relationship with China due to trust issues. Cybersecurity, political intervention by the Chinese state and uneven access to their markets is causing the West to re-evaluate our relationship. This will mean that companies will try to find other options such as reshoring manufacturing. This will lead to higher prices.

4. ESG (Environmental Social Governance), Social Lending, Justice and Green Programs

This type of policy is now in vogue. Even though it is just and honourable to consider these social lending polices, from an economic perspective the policies will force higher prices since these policies have a cost which must be shared throughout society.

5. Central Banks’ Policies Mandate Inflation

Most central banks have abandoned low inflation policy. The US Federal Reserve has now installed a policy where inflation targets should be at minimum 2%. Central banks have said they will not tighten monetary policy until they see a complete recovery.

6. Asset Prices Are Now Inflationary

Whether it is housing, the stock market or bitcoin, all asset classes are now reaching bubbling levels that will trickle down into the Consumer Price Index (CPI) inflation calculation.

7. Interest Rate Curve Suppression (Not Happened Yet)

There has been recent discussion on central banks trying to control and pin down long-term interest rates by purchasing unlimited amounts of bonds to keep the interest rate curve low. If this does happen, inflation will certainly rise.

8. Macro Prudential Regulation (Not Happened Yet)

As previously mentioned, central banks will be pressured politically. The main issue is that money expansion is not getting to the consumer or small business. There is early talk that governments could force banks to lend by guaranteeing all loans to their customers. Or governments could force their central banks to buy outstanding federal debt, thereby creating money by fiat. (Most modern currencies are fiat or paper currencies that are not based on a commodity such as gold.) Regardless, if this does happen, inflation becomes a real issue.

In Summary

We do believe reflation is on the horizon. We believe that inflation will easily move from 1.5% to potentially 3.0% in six months. Over time, we think that higher inflation is a bigger risk than lower inflation. If that occurs, it is a headwind for the bond portfolio.

With this in mind, we have been in a defensive mode since mid-2020 with our bond portfolio by doing the following:

- Lower term-to-maturity (shorter duration): 3.5 years versus 7 years for the index

- Credit exposure primarily in the 1 to 3 year area

- Larger weight towards REITs – sector trades at a discount to its Net Asset Value

- Lower weight to High Yield – sector shows little value versus risk.

- Possible purchase of inflation index-linked bonds in near future.

(As a reminder we can own 20% of the bond portfolio in higher risk assets such as convertibles, real estate investment trusts, preferred shares, and non-investment grade bonds.)